Select Energy Services Reports Fourth Quarter and Fiscal Year 2018 Financial Results & Operational Updates

Feb 26, 2019

HOUSTON, Feb. 26, 2019 /PRNewswire/ — Select Energy Services, Inc. (NYSE: WTTR) (“Select” or “the Company”), a leading provider of water management and chemical solutions to the North American unconventional oil and gas industry, today announced results for the fourth quarter and fiscal year ended December 31, 2018.

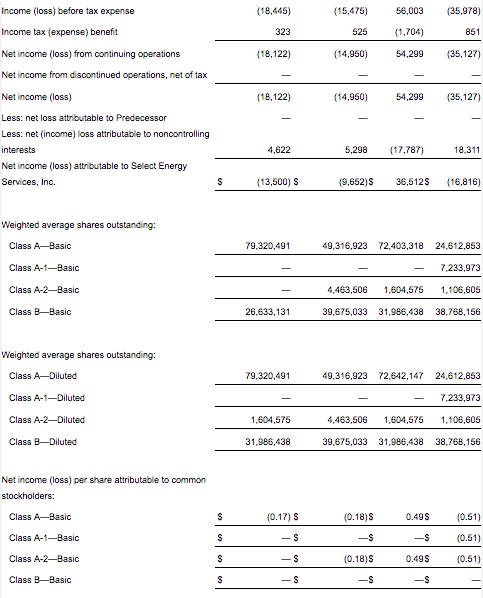

Revenue for fiscal year 2018 was $1,528.9 million as compared to $692.5 million in fiscal year 2017. Revenue for the fourth quarter of 2018 was $362.3 million as compared to $397.0 million in the third quarter of 2018 and $304.2 million in the fourth quarter of 2017. Net income for fiscal year 2018 was $54.3 million as compared to a net loss of $35.1 million in fiscal year 2017. Net loss for the fourth quarter of 2018 was $18.1 million, driven in part by a number of non-recurring charges as detailed below, compared to net income of $31.3 million in the third quarter of 2018 and a net loss of $15.0 million in the fourth quarter of 2017.

Holli Ladhani, President and CEO, stated, “The team executed on our commitment to deliver strong cash flow and manage operations through the anticipated, but challenging, activity decline as the year ended. With over $100 million of operating cash flow in the quarter, we were able to fund our capital program, pay for a small but strategic acquisition in New Mexico, execute a modest share repurchase initiative and reduce our borrowings. Additionally, we’ve commenced construction of a new pre-frac water delivery pipeline in the Northern Delaware Basin of New Mexico, which will expand our already substantial footprint in the region. This project is supported by a 5-year take-or-pay contract with a major international integrated oil company. With this investment, which we expect to fund with proceeds from the sale of portions of our Wellsite Services business, we have now committed over $85 million to water infrastructure alone in the Northern Delaware Basin.

“The Northern Delaware Basin infrastructure project further exemplifies the strength of the Select team in developing long-term value-added solutions for our customers. We believe funding this system through the divestment of non-core operations provides an efficient opportunity to reallocate our capital towards higher margin, more stable cash flow streams. Also, the share repurchase exhibits the importance of returning capital to shareholders as an important part of our overall capital allocation strategy and we will continue to evaluate capital return opportunities during 2019.

“While the activity outlook for 2019 remains somewhat uncertain, we are confident the United States will remain the center of long-term global supply growth and the demand for water-related services will continue to grow. We are well positioned to support our customers in 2019 and expect to generate cash flow in excess of our 2018 levels. We will generate this free cash flow by remaining focused on developing our comprehensive water solutions strategy and managing our variable costs. Where appropriate, we will continue evaluating investments in infrastructure, as well as in technologies such as automation that support our operational efficiency initiatives, all while keeping a disciplined approach to capital allocation,” concluded Ladhani.

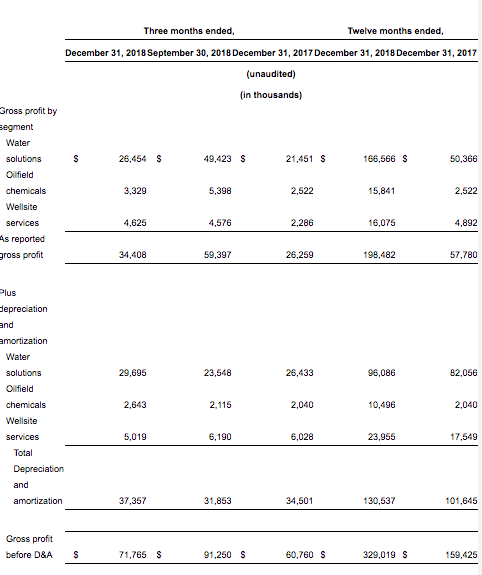

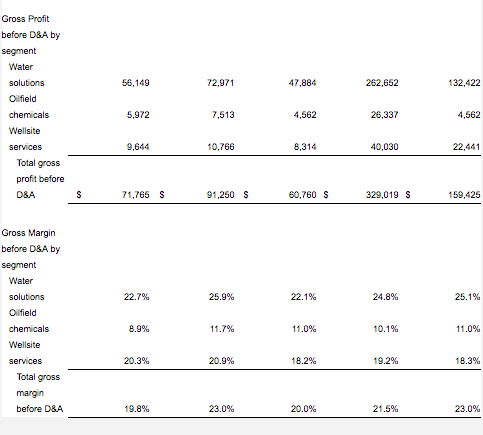

Gross profit was $34.4 million in the fourth quarter of 2018 as compared to $59.4 million in the third quarter of 2018 and $26.3 million in the fourth quarter of 2017. Total gross margin for Select was 9.5% in the fourth quarter of 2018 as compared to 15.0% in the third quarter of 2018 and 8.6% in the fourth quarter of 2017. Gross margin before depreciation and amortization (“D&A”) for the fourth quarter of 2018 was 19.8% as compared to 23.0% for the third quarter of 2018 and 20.0% for the fourth quarter of 2017.

Gross profit for fiscal year 2018 was $198.5 million as compared to $57.8 million in fiscal year 2017, and gross margin was 13.0% in fiscal year 2018 as compared to 8.3% in fiscal year 2017. Gross margin before D&A for fiscal year 2018 was 21.5% as compared to 23.0% for fiscal year 2017.

Adjusted EBITDA was $56.1 million or 15.5% of revenue in the fourth quarter of 2018 as compared to $73.7 million or 18.6% of revenue in the third quarter of 2018 and $43.9 million or 14.4% of revenue in the fourth quarter of 2017. Adjusted EBITDA for fiscal year 2018 was $257.6 million as compared to $117.3 million in fiscal year 2017. Please refer to the reconciliations of gross profit before D&A (a non-GAAP measure) to gross profit and of Adjusted EBITDA (a non-GAAP measure) to net income at the end of this news release.

Business Segment Information

The Water Solutions segment generated revenues of $247.5 million in the fourth quarter of 2018 as compared to revenues of $281.4 million in the third quarter of 2018 and $217.0 million in the fourth quarter of 2017. This sequential decline in revenue was driven primarily by decreased well completions in the fourth quarter compared to the prior quarter, which impacted most areas of operations. Gross margin before D&A for Water Solutions was 22.7% in the fourth quarter of 2018 as compared to 25.9% in the third quarter of 2018 and 22.1% in the fourth quarter of 2017. Water Solutions gross margin before D&A was impacted by a $2.1 million non-cash accrual related to a vacation policy change during the fourth quarter. This policy change was put in place as part of the Company’s ongoing retention initiatives to allow for the carryover of unused vacation days into the following calendar year, and impacted other segments as well for a total charge of $2.9 million across the company.

The Oilfield Chemicals segment, which operates through our subsidiary Rockwater Energy Solutions, generated revenues of $67.4 million in the fourth quarter of 2018 as compared to $64.0 million in the third quarter of 2018 and $41.6 million in the fourth quarter of 2017. Gross margin before D&A for Oilfield Chemicals was 8.9% in the fourth quarter of 2018 as compared to 11.7% in the third quarter of 2018 and 11.0% in the fourth quarter of 2017. The segment continued to see strong demand for friction reducer product lines, including its new high-viscosity product, which helped drive an increase in revenues of 5% relative to the third quarter of 2018 despite slower completions activity in the fourth quarter of 2018. While management was pleased with revenue growth, the segment did see a decrease in the gross margin primarily related to increased raw material costs, including recently implemented tariffs, of $1.4 million.

The Wellsite Services segment generated revenues of $47.4 million in the fourth quarter of 2018 as compared to $51.6 million in the third quarter of 2018 and $45.6 million in the fourth quarter of 2017. Gross margin before D&A for Wellsite Services was 20.3% in the fourth quarter of 2018 as compared to 20.9% in the third quarter of 2018 and 18.2% in the fourth quarter of 2017. The segment saw sequential revenue declines of approximately 8% in the fourth quarter largely driven by declines in wellsite construction and sand and fluids hauling businesses. However, the segment held a steady margin profile led by the strength of Peak, Select’s rentals business, which modestly increased revenue during the quarter and grew gross profit before D&A by 7%. Going forward, this segment will be significantly impacted by the expected divestitures of the Company’s wellsite construction business as well as its Canadian water services business.

Select’s consolidated Adjusted EBITDA during the quarter includes adjustments for certain non-recurring and non-cash items including $22.3 million of impairments, made up of a $17.9 million goodwill impairment within its Affirm and Oilfield Chemicals businesses, primarily driven by the decline in external market conditions at year-end, and $4.4 million of asset impairments related to the Company’s Canadian operations. Other adjustments included $4.3 million of non-recurring costs resulting from sales tax audits for the prior years 2011 – 2017, including for acquired businesses such as Rockwater and Crescent, as well as the $2.9 million non-cash, non-recurring charge related to the change in vacation policy, $1.7 million of losses on asset sales, $0.8 million of foreign currency impact and $0.7 million of severance expense. Non-cash compensation expense accounted for an additional $2.3 million adjustment, and other items produced a net impact of ($0.2) million.

Select’s consolidated and Segment results noted above for 2018 include full-quarter contributions from Rockwater Energy Solutions, which Select acquired in November 2017; as such, these results are only included for a portion of the fourth quarter of 2017 and therefore are not directly comparable.

Cash Flow and Balance Sheet

Cash flow from operations for fiscal year 2018 was $232.4 million, of which $107.8 million was generated in the fourth quarter of 2018. Improvements in our working capital management supported the cash flow generated by the business. Capital expenditures for fiscal year 2018 were $151.4 million, net of asset sales of $14.0 million, of which $51.2 million was spent in the fourth quarter of 2018. Cash flow from operations less net capital expenditures was $81.0 million for fiscal 2018 and $56.6 million during the fourth quarter.

Other cash uses, before debt repayment, during the fourth quarter included $15.7 million to fund the repurchase of 1.7 million shares of our Class A common stock and $15.0 million for acquisitions, including $12.4 million for Pro Well Testing and Wireline, Inc. (“Pro Well”), a regional flowback and well testing operator in the Northern Delaware Basin, which expanded our flowback business into a new geography in New Mexico.

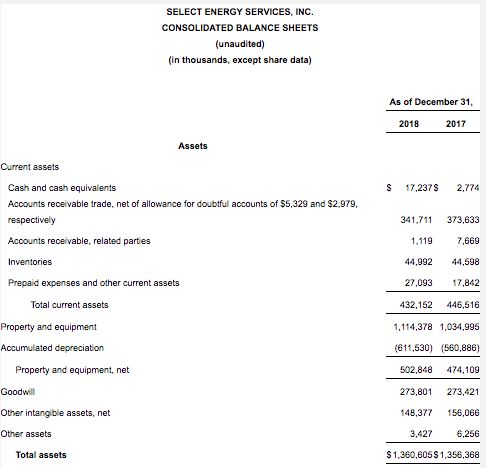

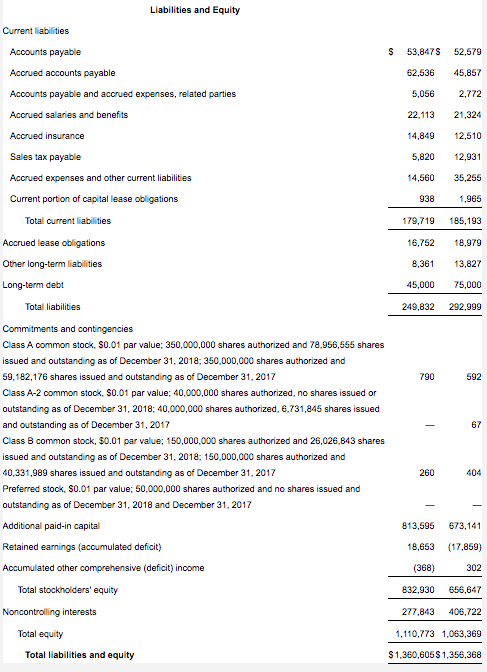

Total liquidity was $221.9 million as of December 31, 2018, as compared to $218.1 million as of September 30, 2018. Outstanding borrowings under the Company’s revolving credit facility totaled $45.0 million as of December 31, 2018, compared to $65.0 million as of September 30, 2018. As of December 31, 2018, the Company had approximately $205.0 million of available borrowing capacity under its revolving credit facility, after giving effect to $20.8 million of outstanding letters of credit. Total cash and cash equivalents were $17.2 million at December 31, 2018, as compared to $13.0 million at September 30, 2018.

Conference Call

Select has scheduled a conference call on Wednesday, February 27, 2019, at 10:00 a.m. Eastern time / 9:00 a.m. Central time. Please dial 201-389-0872 and ask for the Select Energy Services call at least 10 minutes prior to the start time of the call, or listen to the call live over the Internet by logging on to the website at the address http://investors.selectenergyservices.com/events-and-presentations. A telephonic replay of the conference call will be available through March 6, 2019, and may be accessed by calling 201-612-7415 using passcode 13687413#. A webcast archive will also be available at the link above shortly after the call and will be accessible for approximately 90 days.

About Select Energy Services, Inc.

Select is a leading provider of water management and chemical solutions to the North American unconventional oil and gas industry. Select provides for the sourcing and transfer of water, both by permanent pipeline and temporary hose, prior to its use in the drilling and completion activities associated with hydraulic fracturing, as well as complementary water-related services that support oil and gas well completion and production activities, including containment, monitoring, treatment and recycling, flowback, hauling, and disposal. Select, under its Rockwater Energy Solutions subsidiary, develops and manufactures a full suite of specialty chemicals used in the well completion process and production chemicals used to enhance performance over the producing life of a well. Select currently provides services to exploration and production companies and oilfield service companies operating in all the major shale and producing basins in the United States and Western Canada. For more information, please visit Select’s website, https://www.selectenergy.com.

Cautionary Statement Regarding Forward-Looking Statements

All statements in this communication other than statements of historical facts are forward-looking statements which contain our current expectations about our future results. We have attempted to identify any forward-looking statements by using words such as “expect,” “will,” “estimate” and other similar expressions. Although we believe that the expectations reflected, and the assumptions or bases underlying our forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Such statements are not guarantees of future performance or events and are subject to known and unknown risks and uncertainties that could cause our actual results, events or financial positions to differ materially from those included within or implied by such forward-looking statements. Factors that could materially impact such forward-looking statements include, but are not limited to, the factors discussed or referenced in the “Risk Factors” section of our Annual Report on Form 10-K for the year ended December 31, 2017, and in any subsequently filed quarterly reports on Form 10-Q or current reports on Form 8-K. Investors should not place undue reliance on our forward-looking statements. Any forward-looking statement speaks only as of the date on which such statement is made, and we undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events, changed circumstances or otherwise, unless required by law.

WTTR-ER

Comparison of Non-GAAP Financial Measures

EBITDA, Adjusted EBITDA, gross profit before depreciation and amortization (D&A) and gross margin before D&A are not financial measures presented in accordance with GAAP. We define EBITDA as net income, plus interest expense, taxes and depreciation & amortization. We define Adjusted EBITDA as EBITDA plus/(minus) loss/(income) from discontinued operations, plus any impairment charges or asset write-offs pursuant to GAAP, plus/(minus) non-cash losses/(gains) on the sale of assets or subsidiaries, non-recurring compensation expense, non-cash compensation expense, and non-recurring or unusual expenses or charges, including severance expenses, transaction costs, or facilities-related exit and disposal-related expenditures, plus/(minus) foreign currency losses/(gains) and plus any inventory write-downs. We define gross profit before D&A as revenue less cost of revenue, excluding cost of sales D&A expense. We define gross margin before D&A as gross profit before D&A divided by revenue. EBITDA, Adjusted EBITDA, gross profit before D&A and gross margin before D&A are supplemental non-GAAP financial measures that we believe provide useful information to external users of our financial statements, such as industry analysts, investors, lenders and rating agencies because it allows them to compare our operating performance on a consistent basis across periods by removing the effects of our capital structure (such as varying levels of interest expense), asset base (such as depreciation and amortization) and non-recurring items outside the control of our management team. We present EBITDA, Adjusted EBITDA, gross profit before D&A and gross margin before D&A because we believe they provide useful information regarding the factors and trends affecting our business in addition to measures calculated under GAAP.

Net income is the GAAP measure most directly comparable to EBITDA and Adjusted EBITDA. Gross profit is the GAAP measure most directly comparable to gross profit before D&A. Our non-GAAP financial measures should not be considered as alternatives to the most directly comparable GAAP financial measure. Each of these non-GAAP financial measures has important limitations as an analytical tool due to exclusion of some but not all items that affect the most directly comparable GAAP financial measures. You should not consider EBITDA, Adjusted EBITDA or gross profit before D&A in isolation or as substitutes for an analysis of our results as reported under GAAP. Because EBITDA, Adjusted EBITDA and gross profit before D&A may be defined differently by other companies in our industry, our definitions of these non-GAAP financial measures may not be comparable to similarly titled measures of other companies, thereby diminishing their utility. For further discussion, please see “Item 6. Selected Financial Data” in our Annual Report on Form 10-K for the year ended December 31, 2017.

The following tables present a reconciliation of EBITDA and Adjusted EBITDA to our net income (loss), which is the most directly comparable GAAP measure for the periods presented:

Contacts:

Select Energy Services

Chris George, VP, Investor Relations & Treasurer

(713)296-1073

IR@selectenergyservices.com

Dennard – Lascar Associates

Ken Dennard / Lisa Elliott

(713)529-6600

WTTR@dennardlascar.com

View original content:http://www.prnewswire.com/news-releases/select-energy-services-reports-fourth-quarter-and-fiscal-year-2018-financial-results-and-operational-updates-300802818.html

SOURCE Select Energy Services, Inc.